Investors Are Not Ready for What 2026 May Bring

AI disruption, a weakening labor market, and the silent battle over corporate margins Introduction: Why 2026 Matters More Than It Seems Financial markets rarely collapse without warning. More often, they reprice reality gradually, long before the macro headlines turn alarming. What many investors currently describe as “temporary volatility” or “sector rotation” may in fact be the early stages of a deeper structural shift. As we move closer to 2026, multiple stress factors are converging at the same time. Not in consumer demand, not in inflation alone, but in the most fragile part of the corporate system: profit margins. This is not a story about panic.It is a story about mispricing risk. 1️⃣ Two Structural Pressures Hitting Markets Simultaneously 🔹 The Technological Shock: AI Is No Longer a Theme — It’s a Competitor Artificial intelligence has moved far beyond being a speculative growth narrative for tech stocks. It is now directly competing with human labor, including in areas once considered immune: The result is not just higher productivity.It is downward pressure on pricing power. Business models that relied on expensive human expertise are being challenged. In many sectors, AI does not need to be perfect — it only needs to be good enough and dramatically cheaper. That has profound implications for margins. 🔹 The Economic Shift: A Turning Point in the U.S. Labor Market Historically, equity markets tend to ignore labor market weakness — until they can’t. Recent data suggests a clear change in corporate behavior: When companies stop hiring, earnings growth usually follows with a delay.Markets tend to react late, not early. 2️⃣ Why Corporations Are Cutting Jobs — The Real Reasons Publicly, layoffs are framed as efficiency measures. Privately, the drivers are more structural: Major corporations are committing hundreds of billions of dollars to data centers, chips, and AI infrastructure. That capital must come from somewhere — and labor costs are the easiest lever to pull. This is not a short-term adjustment.It is a reallocation of capital priorities. 3️⃣ What Market Behavior Is Telling Us (Beyond Individual Stocks) Rather than focusing on specific companies, it is more useful to observe how capital is behaving: This pattern is consistent with previous late-cycle environments — not crashes, but transitions. 4️⃣ The Investment Mindset Required for 2026 ✔ Patience Only Works If the Business Model Survives Waiting for a recovery makes sense only if the underlying business remains relevant. Low valuation alone is not protection if: Many industries once looked “cheap” for good reason. ✔ Resilience Matters More Than Valuation Multiples In an AI-driven, slowing economy, the most important traits are: Cheap but fragile companies tend to stay cheap — or fail. ✔ A Portfolio Is a System, Not a Collection Every position should have a role: Owning dozens of positions without a clear purpose is not diversification.It is unmanaged risk. 5️⃣ Outlook for 2026: Collapse or Repricing? An immediate, systemic collapse remains unlikely. A more realistic scenario includes: U.S. corporations are still profitable.The question is not if earnings fall — but which businesses can adapt. Conclusion – The Cartwright Capital View 2026 is unlikely to reward impatience. This cycle favors investors who understand: Artificial intelligence is not just a growth catalyst.It is a stress test for business models. And stress tests reveal weaknesses long before markets fully price them in. Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions. Sources

Is the AI Bubble About to Burst — or Are We Still Early in the Cycle?

Artificial intelligence has become the defining investment theme of this market cycle. Over the past two years, AI-related stocks have delivered outsized returns, valuations have expanded rapidly, and capital has concentrated into a very narrow segment of the equity market. As a result, investors are increasingly asking a critical question: are we witnessing the formation of an AI bubble — and if so, what happens next? This article takes a measured, analytical view, in line with the Cartwright Capital philosophy. Rather than chasing headlines, we focus on fundamentals, capital flows, valuation discipline, and historical context. AI is not evaluated as a slogan, but as an economic force — one that can create long-term value while simultaneously producing short-term excess. Why the AI Bubble Debate Matters Right Now AI is no longer speculative technology. It is actively reshaping cloud computing, enterprise software, advertising, logistics, healthcare, and defense. At the same time, hundreds of billions of dollars are being deployed into AI infrastructure, chips, data centers, and model development. Yet markets are displaying classic late-cycle characteristics: These signals do not imply an imminent crash — but they raise the probability of mispricing. AI Is Real — But Not Every Valuation Is A crucial distinction must be made early: AI itself is not a bubble. Unlike the dot-com era, today’s AI leaders generate: The risk lies elsewhere — in expectations embedded in prices. Many stocks are being valued not on current cash flows, but on optimistic assumptions about growth five to ten years into the future, with little margin for error. From a fundamental perspective, the danger zone appears when: History suggests such assumptions rarely hold indefinitely. Valuations and Market Psychology In parts of the AI ecosystem, we see: Markets are implicitly pricing in a scenario where AI investment demand remains strong regardless of economic conditions. That may prove optimistic. Capital-intensive technologies tend to experience periods of overinvestment followed by normalization — and AI will not be immune. Bull vs. Bear Case for AI The Bull Case The Bear Case The most likely outcome lies between these extremes. The Magnificent Seven: Market Engine and Systemic Risk A central reason the AI bubble debate exists at all is the extraordinary dominance of the Magnificent Seven: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla. These companies no longer merely represent the technology sector — they effectively define the equity market’s direction. Over the past cycle, a disproportionate share of S&P 500 and Nasdaq gains has been driven by this small group. Concentration alone is not inherently dangerous. What matters is how capital behaves inside this concentration. How Capital Circulates Within the Magnificent Seven Rather than traditional sector rotation, today’s market increasingly exhibits internal rotation within Big Tech itself. A common pattern: The result is a market that appears healthy at the index level while participation narrows underneath. The AI Capital Feedback Loop One of the most distinctive features of this cycle is that the Magnificent Seven reinforce each other’s growth: This creates a positive feedback loop — powerful, but inherently fragile. If: the loop can reverse faster than expected. Not Dot-Com — But Late-Cycle Behavior It is critical to avoid false analogies. The Magnificent Seven are not speculative startups. They generate enormous cash flow and control essential digital infrastructure. However, the resemblance to past bubbles lies in expectation concentration, not business quality. Markets currently assume: Historically, technology cycles rarely conclude with permanent dominance by a fixed group. What Happens If One Link Breaks? The Magnificent Seven are now sentiment-linked. A meaningful disappointment from: would likely trigger basket-level selling. Passive flows, ETFs, and systematic strategies treat these stocks as a single exposure. The result would not reflect collapsing fundamentals — but rather risk repricing. Three Plausible Scenarios Ahead Conservative Scenario AI remains a structural trend, but capital rotates away from weaker names. Valuations compress while leaders survive. Base Case Markets experience a healthy correction, separating durable cash-flow generators from speculative narratives. Negative Scenario A macro shock accelerates risk-off behavior, with AI acting as the catalyst rather than the cause. The Cartwright Capital View From an investment standpoint, Cartwright Capital sees no evidence that AI itself is a bubble. What exists instead is selective excess, driven by capital concentration and unrealistic expectations. AI will likely reshape productivity and profitability over the next decade. But returns will not be evenly distributed — nor will they follow a straight line. The real risk is not technological failure.It is overconfidence in valuation permanence. Disciplined investors should focus on: If an AI bubble exists, it is not in the technology, but in the belief that today’s capital concentration can persist indefinitely. Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions. Sources

Why Did Markets Fall This Week? Politics, the Fed, and a Reality Check on Risk

Global equity markets had a weak week, reminding investors that 2026 is unlikely to be a smooth, one-directional rally. The sell-off was not triggered by a single dramatic event. Instead, it was driven by a combination of political uncertainty, monetary policy expectations, and a long-overdue reassessment of risk. Here are the key factors behind the move. 1️⃣ Politics: Trump Back in the Market Narrative One of the main sources of renewed uncertainty is the growing political relevance of Donald Trump. Markets are not reacting to polling numbers alone, but to the implications of a realistic Trump return to power. Investors are increasingly pricing in: Markets dislike uncertainty more than bad news. A wider range of political outcomes automatically means a higher risk premium for equities. 2️⃣ The Federal Reserve: Higher Rates for Longer Another critical factor was communication from the Federal Reserve. While no new Fed leadership has been appointed, the tone of recent messaging has been enough to unsettle markets. The key takeaway: This matters because: 3️⃣ Bond Markets Are Sending a Warning One of the strongest signals did not come from equities, but from bonds. In simple terms:👉 capital is no longer cheap👉 risk assets must adjust Equities are now catching up with what bond markets have been signaling for weeks. 4️⃣ Valuations Were Stretched It is important to keep context in mind. Markets had rallied strongly before this pullback. Once higher rates and political uncertainty re-entered the equation, profit-taking was inevitable. This was not panic selling—it was a rational reset. 5️⃣ Market Psychology: From Optimism to Caution Markets move in cycles: The current phase reflects a shift away from narratives and toward fundamentals: This transition tends to be uncomfortable—but healthy. What This Means for Investors 👉 This does not signal the end of the bull market, but rather a change in regime.👉 In 2026, politics and central banks will matter as much as corporate earnings.👉 Quality, diversification, and cash flow are back in focus. Assets such as gold, defensive equities, dividend payers, and companies with strong balance sheets are regaining relevance. Blindly chasing growth without regard to valuation or rates carries increasing risk. Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions. Sources & References

Key Earnings Highlights: What Major Corporations Revealed on January 28–29, 2026

Date: January 28–29, 2026 The final days of January brought one of the most closely watched earnings windows of the quarter. Several global market leaders across technology, semiconductors, automotive, media, and communications reported their latest results, offering valuable insight into corporate profitability, capital allocation, and strategic direction as we enter 2026. Companies such as ASML, Tesla, Meta Platforms, Microsoft, Comcast, and Apple collectively shape investor sentiment—and their earnings this week clearly underline one dominant theme: AI-driven investment and capital intensity are redefining the market landscape. Below is a structured overview of the most important earnings releases from January 28–29, 2026. ASML (ASML) – Semiconductor Backbone of the AI Cycle Reported: January 28, 2026 (Pre-Market) ASML delivered one of the strongest reports of the season, confirming its role as a critical supplier to the global semiconductor ecosystem. ASML also announced an expanded share buyback program totaling €12 billion and increased shareholder returns via dividends. Cartwright Capital view:ASML’s results confirm that AI-driven demand is not a short-term narrative but a structural trend. The company’s backlog and forward guidance provide rare visibility in an otherwise uncertain macro environment. Tesla (TSLA) – Transition Phase Between EVs and AI Reported: January 28, 2026 (After Market Close) Tesla’s results exceeded consensus expectations but highlighted an ongoing transition in its business model. Management emphasized continued investment in autonomous driving, robotics, and AI infrastructure, while traditional EV growth remains under pressure. Cartwright Capital view:Tesla is increasingly valued less as a pure automotive company and more as a long-duration AI and energy platform. Execution risk remains, but strategic optionality is significant. Meta Platforms (META) – AI at Full Scale Reported: January 28–29, 2026 Meta delivered a standout earnings report, beating expectations on both revenue and profitability. The company continues to benefit from strong advertising demand while aggressively scaling AI infrastructure. Cartwright Capital view:Meta’s earnings reinforce a clear message: advertising monetization and AI investment are no longer competing priorities—they are mutually reinforcing. Microsoft (MSFT) – Strong Numbers, Cautious Market Reaction Reported: January 28, 2026 (After Market Close) Microsoft once again posted solid financial results, though market reaction was mixed. Despite operational strength, investors remain sensitive to capital intensity and near-term margin dynamics. Cartwright Capital view:Microsoft remains one of the most strategically positioned AI platforms globally. Short-term margin concerns do little to undermine its long-term competitive moat. Comcast (CMCSA) – Cash Flow Strength Amid Mixed Operations Reported: January 29, 2026 (Pre-Market) Comcast delivered a mixed earnings report, highlighted by strong cash generation. Growth in wireless services and theme parks partially offset pressure in legacy segments. Cartwright Capital view:Comcast remains a cash-generating machine, but structural challenges in media and broadband competition continue to cap valuation upside. Apple (AAPL) – Earnings That Carry the Entire Market Reported: January 29, 2026 (After Market Close) Apple’s fiscal Q1 results were released after market close, making this one of the most anticipated earnings events of the season. Apple’s earnings traditionally act as a macro signal for global consumer demand. Cartwright Capital view:With expectations extremely high, Apple’s results matter not just for its shareholders, but for overall market sentiment entering Q1 2026. Key Takeaways for Investors Final Thoughts The earnings releases of January 28–29, 2026 confirm that markets are entering a phase where capital discipline, AI infrastructure, and long-term strategic positioning matter more than short-term margin fluctuations. While not all companies delivered flawless results, the broader message is clear: corporate America is betting heavily on AI—and investors must decide which balance sheets can support that bet sustainably. Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions.

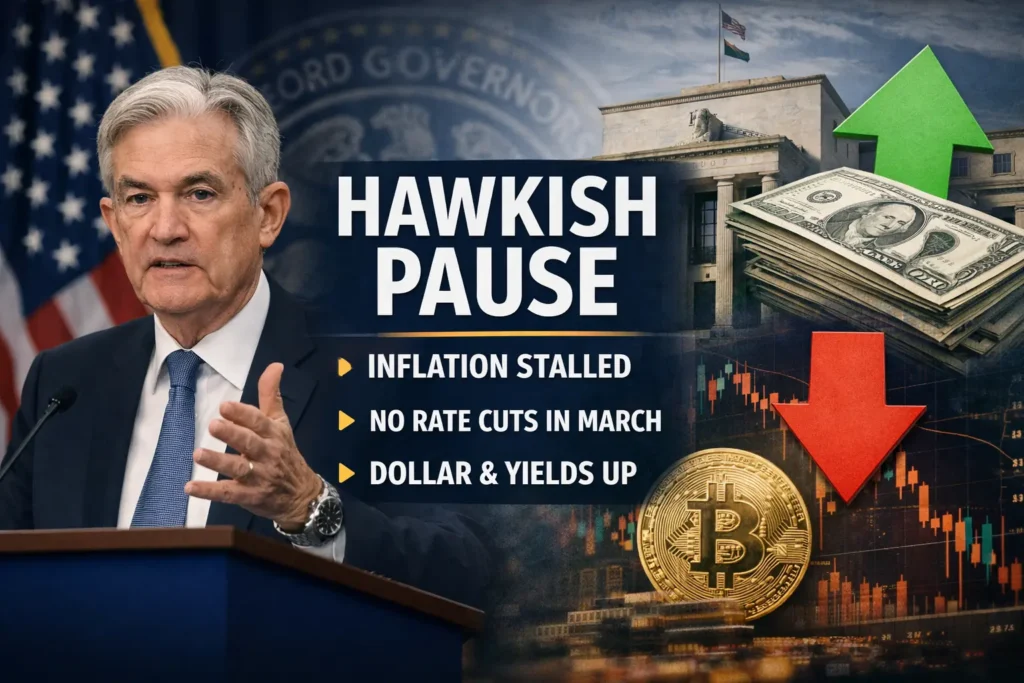

Fed Holds Rates, Tightens the Message: A Hawkish Pause That Resets Market Expectations

The Federal Reserve left interest rates unchanged at its latest meeting, but the substance of its communication marked a clear shift. While markets had hoped for a confirmation of imminent easing, the Fed delivered something very different: a hawkish pause. In short, rates remain high, liquidity continues to be withdrawn, and the burden of proof has shifted back to the data. Inflation Progress Has Stalled Compared to December, the official FOMC statement included several subtle but important changes. Most notably, the Fed acknowledged that progress toward the 2% inflation target has stalled over the past two months. Instead of continuing lower, inflation has moved sideways. This represents a meaningful change from the autumn narrative, when Chair Jerome Powell spoke about a “clear downward trajectory” in inflation. That confidence is now gone. At the same time, the Fed now views risks to inflation and employment as roughly balanced. Previously, recession risks were seen as dominant. This rebalancing explains why there is no urgency to cut rates. Another key point: quantitative tightening (QT) continues at the same pace. Even without rate hikes, the Fed is actively draining liquidity from the system, reinforcing restrictive financial conditions. Powell’s Press Conference: Caution and Credibility During the press conference, Jerome Powell was careful not to commit to a specific path, but several signals were clear. First, a March rate cut is highly unlikely. Powell repeatedly emphasized the need to see more data from the first quarter, effectively pushing any potential easing decision into May or June at the earliest. Second, Powell strongly defended the Fed’s independence. In response to repeated questions about political pressure, he stressed that the Fed’s mandate is set by law and that short-term political cycles must not interfere with long-term price stability. For investors, this reinforces the Fed’s institutional credibility. Third, Powell highlighted persistent inflation in the services sector. While goods prices are easing, services inflation—particularly rents, insurance, and transportation—remains sticky. This rigidity is now the primary obstacle to a sustained return to the 2% target. Market Reaction: Reality Check Markets reacted immediately to the hawkish tone. The U.S. dollar (DXY) strengthened as higher-for-longer rate expectations increased its relative attractiveness versus Europe and Japan. U.S. 10-year Treasury yields moved back toward 4.2%, reflecting the repricing of rate-cut expectations. Equities declined modestly as investors adjusted models that had assumed faster monetary easing. Bitcoin also moved lower, once again confirming its strong correlation with global liquidity conditions. What Matters Next The Fed has made it clear which data points now matter most: Until then, one message dominates: money remains expensive, liquidity is tight, and discipline matters again. Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions.

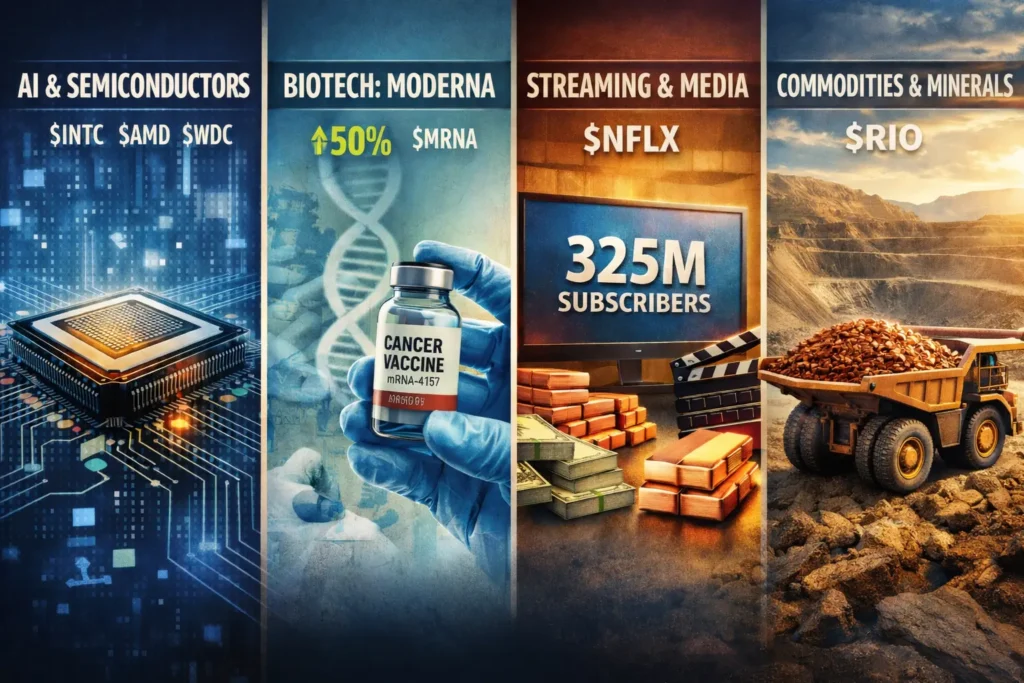

Markets Q1 2026: AI, Data Centers, Healthcare & Media — What Investors Need to Watch

1) Semiconductors & AI — The Bullish Narrative Remains Intact The semiconductor sector continues to sit at the core of global equity market momentum, driven by relentless demand for artificial intelligence computing power. Stocks such as Intel, AMD, and Western Digital have delivered strong recent performance, reflecting sustained optimism around AI infrastructure and hardware demand. 🔍 Why this matters:AI model training, inference, and large-scale deployment are driving exponential growth in demand for high-performance chips, memory, and storage. This is no longer a short-term hype cycle — it is structural. ⚡ Energy: The Hidden Bottleneck of AI A key secondary trend is energy supply for data centers. Hyperscalers such as Amazon and Microsoft are increasingly financing and developing their own power-generation capacity — often directly adjacent to data centers — to secure long-term energy availability for AI workloads. This includes growing interest in nuclear and alternative baseload energy, highlighting an emerging investment theme at the intersection of technology and utilities. 👉 Cartwright Capital insight:Semiconductors and AI infrastructure represent a long-duration growth theme. Investors should think in terms of ecosystems — chips, energy, cooling, and data infrastructure — rather than isolated winners. 2) Healthcare & Biotech — Moderna as a High-Conviction Case Study Moderna emerged as one of the strongest performers following the release of long-term clinical data for its personalized melanoma vaccine developed in partnership with Merck and its flagship oncology drug Keytruda. 📊 Five-year data from Phase II trials indicate approximately a 49–50% reduction in the risk of recurrence or death for high-risk melanoma patients compared with Keytruda alone. 🔬 Why this is significant:This strengthens the investment thesis that mRNA technology can extend far beyond infectious disease vaccines into personalized cancer immunotherapy, opening multi-decade growth opportunities. 👉 Cartwright Capital insight:Biotech remains a high-risk, high-reward space. Companies with validated platforms and strong clinical pipelines — particularly in oncology — deserve close monitoring, but position sizing and risk discipline remain essential. 3) Streaming & Media — Strong Results, Strategic Trade-Offs Netflix continues to demonstrate operational strength: However, management has also signaled higher content spending, which introduces short-term margin pressure despite long-term competitive positioning. 🎬 M&A Spotlight: Warner Bros. Discovery Netflix has reportedly revised its proposal to acquire Warner Bros. Discovery into an all-cash transaction, aimed at reducing uncertainty for WBD shareholders and strengthening negotiating leverage. While such a deal could reshape the global media landscape, it also increases capital allocation risk and regulatory scrutiny. 👉 Cartwright Capital insight:Netflix remains a high-quality asset, but valuation and capital discipline matter. Strategic expansion beyond the core business must be assessed through the lens of long-term shareholder returns. 4) Consumer Goods & Cosmetics — Moats vs. Trends The consumer sector highlights a clear divide between established brands with strong moats and trend-driven challengers. Global leaders such as L’Oréal and Estée Lauder continue to benefit from brand loyalty, pricing power, and scale — particularly in core categories like skincare and makeup. By contrast, color cosmetics and influencer-driven brands remain highly volatile, often dependent on social media platforms such as TikTok, where trends can reverse rapidly. 👉 Cartwright Capital insight:In consumer sectors, durability of brand equity matters more than short-term growth spikes. Long-term investors should prioritize companies with proven pricing power and repeat customers. 5) Commodities & Materials — Cyclical Strength, Selective Exposure Mining and materials companies such as Rio Tinto are benefiting from solid production results and a favorable outlook for iron ore and copper, supported by electrification and infrastructure demand. That said, materials remain inherently cyclical. 👉 Cartwright Capital insight:Commodities can enhance portfolio diversification, but positions should be sized with full awareness of macroeconomic cycles and volatility. 6) Additional Stock Insights & Investor Q&A 🧠 Kraft Heinz (KHC) Berkshire Hathaway has registered its stake for a potential sale, which markets interpret as a negative signal — possibly an admission that the original investment thesis no longer holds. 🎨 Adobe (ADBE) AI-driven content creation presents both opportunity and disruption. Adobe’s valuation (around ~13x cash flow) already reflects a conservative scenario, but competitive dynamics must be monitored closely. 📚 Duolingo (DUOL) Duolingo maintains a strong competitive edge through gamification and habit formation — elements that current AI chatbots struggle to replicate at scale. 💳 Fiserv A potential turnaround story under new management, though the payments space remains highly competitive with compressed margins. 📌 Final Takeaway for Investors Constructive / Bullish Themes Areas Requiring Caution Disclaimer This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions. Sources