The Federal Reserve left interest rates unchanged at its latest meeting, but the substance of its communication marked a clear shift. While markets had hoped for a confirmation of imminent easing, the Fed delivered something very different: a hawkish pause.

In short, rates remain high, liquidity continues to be withdrawn, and the burden of proof has shifted back to the data.

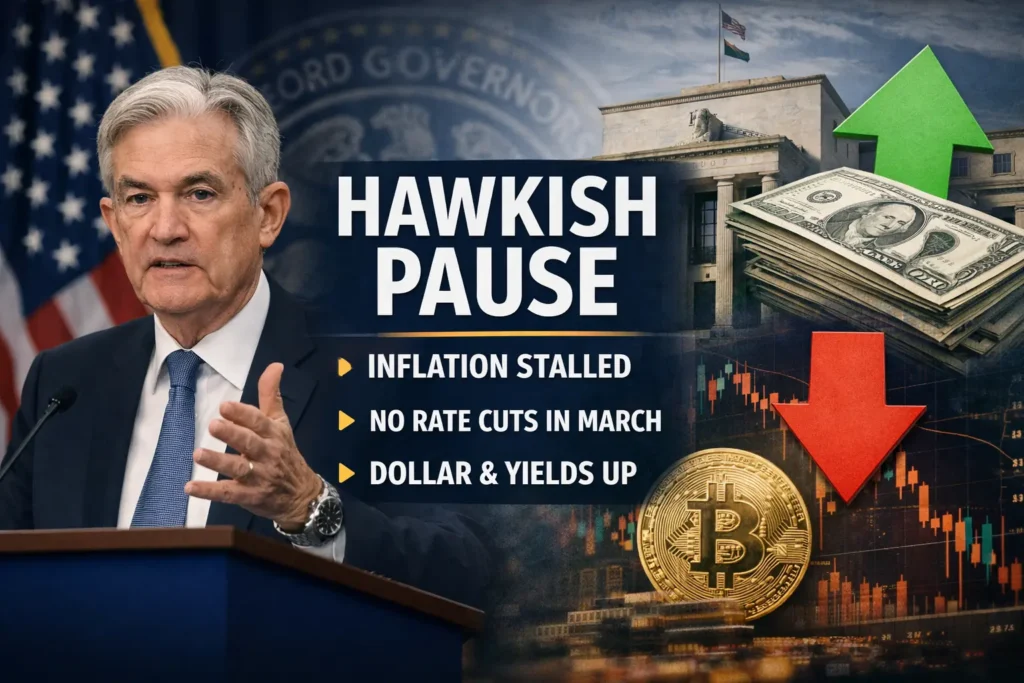

Inflation Progress Has Stalled

Compared to December, the official FOMC statement included several subtle but important changes. Most notably, the Fed acknowledged that progress toward the 2% inflation target has stalled over the past two months. Instead of continuing lower, inflation has moved sideways.

This represents a meaningful change from the autumn narrative, when Chair Jerome Powell spoke about a “clear downward trajectory” in inflation. That confidence is now gone.

At the same time, the Fed now views risks to inflation and employment as roughly balanced. Previously, recession risks were seen as dominant. This rebalancing explains why there is no urgency to cut rates.

Another key point: quantitative tightening (QT) continues at the same pace. Even without rate hikes, the Fed is actively draining liquidity from the system, reinforcing restrictive financial conditions.

Powell’s Press Conference: Caution and Credibility

During the press conference, Jerome Powell was careful not to commit to a specific path, but several signals were clear.

First, a March rate cut is highly unlikely. Powell repeatedly emphasized the need to see more data from the first quarter, effectively pushing any potential easing decision into May or June at the earliest.

Second, Powell strongly defended the Fed’s independence. In response to repeated questions about political pressure, he stressed that the Fed’s mandate is set by law and that short-term political cycles must not interfere with long-term price stability. For investors, this reinforces the Fed’s institutional credibility.

Third, Powell highlighted persistent inflation in the services sector. While goods prices are easing, services inflation—particularly rents, insurance, and transportation—remains sticky. This rigidity is now the primary obstacle to a sustained return to the 2% target.

Market Reaction: Reality Check

Markets reacted immediately to the hawkish tone.

The U.S. dollar (DXY) strengthened as higher-for-longer rate expectations increased its relative attractiveness versus Europe and Japan. U.S. 10-year Treasury yields moved back toward 4.2%, reflecting the repricing of rate-cut expectations.

Equities declined modestly as investors adjusted models that had assumed faster monetary easing. Bitcoin also moved lower, once again confirming its strong correlation with global liquidity conditions.

What Matters Next

The Fed has made it clear which data points now matter most:

- Non-Farm Payrolls (NFP): Any unexpected weakening in the labor market would significantly increase pressure for a rate cut in May or June.

- CPI Inflation: February data will determine whether the recent inflation pause was seasonal—or the start of a more persistent trend.

Until then, one message dominates: money remains expensive, liquidity is tight, and discipline matters again.

Disclaimer

This article reflects the author’s opinions and interpretations of publicly available information. It is not investment advice. Investing in commodities and financial markets involves risk, and readers should conduct their own research or consult a licensed financial advisor before making any investment decisions.